What is cost control in project management?

The budget is one of the most important issues in project management. Each company aims to complete its mission on time and, above all, on budget. Indeed, while cost overruns can hamper the current project, more importantly they also affect the launch of new projects. By controlling costs, we can remedy this situation at an early stage.

Definition of cost control

Cost control in project management is a holistic process that encompasses estimating, monitoring, proactively managing expenditure and preparing for potential financial risks throughout the project lifecycle. This goes beyond simple budget management, including also rigorous planning and the implementation of preventive measures to mitigate risks that could impact project costs and schedule. As a central element of project management, this practice helps to keep expenditure in line with the approved budget, while offering the flexibility needed to adjust trajectories if variations or risks arise, thereby preserving the project’s financial and time resources.

The importance of cost control

Cost control is more than important for any project. It is one of the three essential points that must be respected: deadlines / cost / quality. Logically, it is complicated to bring a project to fruition if you end up realising that the budget allocated to it is insufficient. The losses and damage can be dramatic for a company. It is all the more essential for organisations working on several projects at the same time.

Thanks to a cost estimate carried out in the planning phase, it is possible to strategically organise the project upstream, as well as monitor it by analysing trends, variances, and if necessary implementing corrective measures before a cost overrun drastically affects the project.

9 best practices in cost control

To control costs effectively, there are a few best practices to follow, whatever the size or type of project:

- Accurate cost estimates upstream: detailed cost estimates can be made for every aspect of the project, using historical data from previous similar projects, internal or external expertise, and project management tools.

- Detail the budget: detail the budget for each phase of the project, taking all the parameters into account. That is, the resources and cost of each, the duration, the potential risks, etc.

- Regularly monitor costs: implement budget monitoring mechanisms throughout the project to quickly identify deviations from the initial budget and take corrective action if necessary.

- Manage costs proactively: carefully assess the financial impact of any changes to the project before implementing them, to avoid unplanned expenditure.

- Assess financial risks: identify and assess potential risks that could impact project costs. Develop mitigation plans for these risks to reduce their financial impact.

- Optimise resources: manage the project’s material resources wisely and maximise their use. For human resources, make sure each task is assigned to the right person.

- Communicate transparently: maintain open and transparent communication between project stakeholders on financial aspects, progress and potential challenges, encouraging a collaborative approach to problem-solving.

- Periodically re-evaluate the budget: regularly review actual expenditure against the planned budget. Adapt and reassess the budget and forecasts if necessary in the light of new information or changes in the situation.

- Use project management tools: use project management software such as Oracle Primavera P6 or MS Project to facilitate data collection, analysis and presentation, as well as cost tracking.

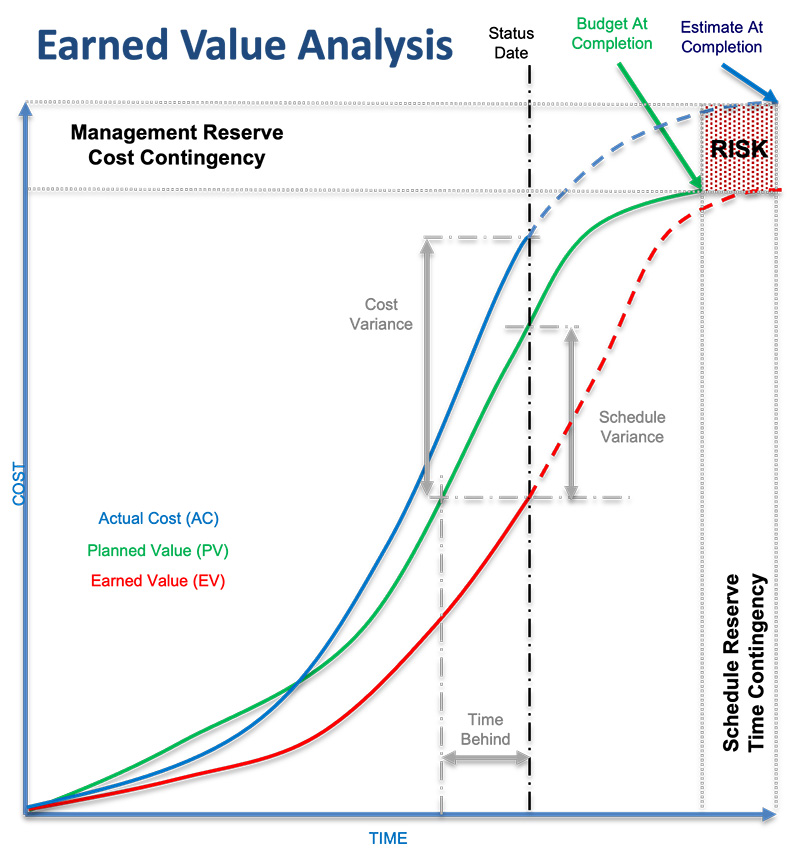

Earned Value Management

Earned Value Management, or EVM, is one of the most widely used cost control methodologies. It is an approach to monitoring and evaluating the performance of a project that integrates costs, deadlines, technical scope and risks. Its purpose is to assess progress against an initial baseline, thereby identifying potential problems and anticipating costs (and to some extent timescales) for completion of the project. To apply EVM, it is crucial to maintain a budget base that is in phase over time. This basis, known as Plan Value (PV) or Budgeted Cost of Work Scheduled (BCWS), is established in stages. Throughout the project, the Cost Performance Index (CPI) will provide a view of the state of the budget.

Earned Value Management enables the project’s performance to be accurately assessed by cross-referencing costs, timescales, technical scope and risks, making it possible to anticipate costs and detect any deviations from the initial plan.

Controlling costs with PROPRISM

However, it is not always easy to apply all this advice proactively. That is why PROPRISM assists its customers in this area. PROPRISM can help you estimate your budget accurately, and also set up an effective budget monitoring system. The aim being to control costs, minimise unforeseen expenditure and optimise the use of resources, thus contributing to the overall success of the project.